r/ukpolitics • u/signed7 • 15h ago

House prices fall again as property market ‘deteriorates’

https://www.cityam.com/house-prices-fall-again-as-property-market-deteriorates/197

u/Izual_Rebirth 15h ago edited 15h ago

We're in a crazy world where both house price increases and house price decreases are met with the same level of negativity, just from different people.

Personally... I'm in a weird situation where we're shared ownership (old model).

If house prices go up then it means the 50% we don't own is more expensive when we come to buy it.

If house prices come down then my LTV on the 50% we do own goes up and gives us less equity towards the other 50% and also potentially will make our mortgage rate more expensive when it comes to renew.

104

u/pancakes1271 Centre Left (Keynesian, Social Democrat) 14h ago

It's not crazy, it's the only way it can be.

Real estate investment is unproductive, zero-sum rent extraction. There cannot be any winners without there being an equal number of losers. The haves and have-nots are completely opposed in their self-interests.

Building so much of our economy and personal finances around real estate was fucking crazy. I don't think you'll find any school of economic thought that thinks more rent-seeking is good for an economy.

•

u/Simple-Courage-3948 9h ago

Rising house prices provide incentives to build more housing, improve existing housing and improve the area where those houses are. The problem is, we don't get all of this because they are regulated and taxed in dumb ways.

•

u/pancakes1271 Centre Left (Keynesian, Social Democrat) 8h ago

That's true, however rent-seekers are directly incentivised to ensure that housing is regulated in such a way as to ensure supply is restricted as much as possible.

→ More replies (5)22

u/TheBearPanda 14h ago

Ideally they’d stay about flat in nominal terms and fall slightly in real terms over time. Makes them more affordable to new buyers without shoving a load of people into negative equity.

5

u/csppr 13h ago

I’m just not sure how stable that can actually be?

The price level of housing over the last years has been significantly propped up by the “housing always goes up” mantra. Once that falls away, hitting the sweet spot of nominal terms stability isn’t exactly an easy balance to strike.

1

u/marsman 12h ago

The price level of housing over the last years has been significantly propped up by the “housing always goes up” mantra.

That's arse about face, prices have increased because more people were chasing the same number of properties and their ability to borrow was better. Prices are broadly set by buyers after all, the 'housing always goes up' element in there is essentially seller expectation, which can impact how many properties are on the market, but not what people are willing to pay for them.

•

u/angryratman 11h ago

I think that's exactly what is going to happen until rates can come down. Any bargains should be at the high-end as people can't afford a £400k mortgage now.

•

u/JibberJim 11h ago

Around me, this is the one area where there are very few bargains - mostly because there's so little supply at that price point because there's nowhere for the people who are selling to buy. So the supply is constrained, cheaper properties are available.

1

u/pslamB 13h ago

While nominal prices are pretty much higher than ever, there has in fact been next to no real house price growth in the past couple of decades (or more if you ignore the pre crisis spike). Mainly as since 2022 it has been a sharp negative overall due to the inflation spike and flatlining nominal prices, before that they were about 10% below their 2007/2008 peak.

4

u/bulldog_blues 13h ago edited 13h ago

What we'd ideally want is for house prices to either stay stagnant OR increase a bit but at a lower rate than wages. That way people who currently own properties can still slowly build up equity, while those looking to buy have a bit more affordability over time.

The problem is that the above takes many years to fully compound, so most people will be dissatisfied with it in some way.

11

u/BobMonkhaus That sounds great, shorty girl’s a trooper. 15h ago

Negative equity is far worse.

7

u/Izual_Rebirth 15h ago edited 14h ago

Luckily not in that situation! But I appreciate for those that are it's a nightmare. I was working at Nationwide on the mortgage desk when the GFC hit and some of the people I had to deal with had were having an awful time. One women I spoke to had something like 110% LTV and they were basically trapped.

Couldn't move onto a FIXED Rate \ TRACKER so were stuck on the Standard Variable Rate which was astronomical at the time - something like 5% BOE base rate + 2% to give you the Nationwide standard variable rate of 7%!. Couldn't move to another mortgage provider as no one would touch negative equity with a barge poll. Gutting.

But for those people looking to get onto the housing market then a drop in house prices might benefit them.

No idea how you ever square the circle of wanting house prices to continue to go up as it's such as important part of our economy while also making them more affordable for first time buyers. Any ideas?

4

u/BobMonkhaus That sounds great, shorty girl’s a trooper. 15h ago

Well since the 2000s massive mortgage fuck up of lending anyone anything and leaving people utterly shafted, they have introduced a lot more regulation into the industry that’s supposed to prevent it happening again.

But then you read that 95% LTV mortgages are available and start to wonder.

4

u/TheFlyingHornet1881 Domino Cummings 13h ago

Even with 95% LTV, after 2 years you'd be fairly unlucky to be in negative equity even with a long mortgage, you'd need house prices to have fallen 7-10%.

14

u/Minute-Improvement57 13h ago

Negative equity is a problem if you have to move house, otherwise it's just regret that you could have paid less later.

9

u/TheFlyingHornet1881 Domino Cummings 13h ago

A big problem though if life circumstances change, I.e redundancy, change in relationship, health issues, or because the negative equity stems from issues near the property that created negative equity.

•

u/Aresbanez 11h ago

Those circumstances should be taken into account before you make a purchase. Nobody should assume the next 20 years are going to be smooth sailing, least of all millennials.

6

u/RiceeeChrispies 13h ago

it's still a problem because you become a mortgage prisoner and get shafted by the SVR.

8

u/Minute-Improvement57 13h ago

Inflation is 2.8%. Even if you're in negative equity by 5%, you're out of your "mortgage prison" in 2 years. The reported fall is 0.6%.

1

u/alba_Phenom 12h ago

That's what I was thinking, you already had the intention of paying the same amount, more or less, for 25 years... if you sell and want to relocate, the value of the next house you're buying is lower.

2

u/Complex_Effect_1994 13h ago

That's only really an issue with a crash. With a small drop, you'll pay off enough of the mortgage per year to not be in negative equity.

And what you lost in house price you gain when the place you want to move to is also cheaper.

•

u/Working_Location_127 8h ago

Real estate is cyclical, if we meet our house building goals prices will likely slump in real terms

1

u/One-Network5160 14h ago

We're in a crazy world where both house price increases and house price decreases are met with the same level of negativity, just from different people.

Well yeah, there's nothing crazy about that. Different people have different opinions depending on their life circumstances.

1

u/Izual_Rebirth 13h ago

True. I could have expanded. I think it puts the government in a really awkward situation. No matter who is in charge, no matter what happens the papers will fear monger one way or the other.

180

u/generichandel 15h ago

Nearly 13% of our economy is based off of swapping houses with each other. This'll be interesting.

35

u/Monsoon_Storm 14h ago

It's something we need to change. We've swapped out productive industry for owning land.

Christ knows it won't though.

42

u/AkashicLogos 15h ago

It makes me laugh that people cheer a housing crash, not understanding what it'd do to the economy & their own finances.

Houses won't magically become absolute bargains. Everyone will suffer.

Lest we forget that 2008 was triggered by a housing crash

49

u/generichandel 15h ago

Oh believe me I'm not cheering it at all. I'm in the worst of the worst situations for it, 4 years into my first mortgage on a sodding leasehold two bedroom flat. I just say "this'll be interesting" because what else can you do?

3

u/92mac 14h ago

Could be worse, could be a 1 bed flat (me) :)

10

u/generichandel 14h ago

Hunker down, nail your door shut, stop paying your service charge, declare your flat an autonomous republic. That way only the foreign office can interact with you when it comes time to sell. A bulletproof plan.

10

u/AkashicLogos 15h ago

I just locked in a 3.93% mortgage before the rate rises so am feeling comfy but I am way more worried about wider economic effects than I am about the price of my house.

1

u/IHateFACSCantos 12h ago

Yes we locked in at 4.23% for 5 years, and I'm much more worried about losing my job again. I was made redundant last year in the wake of the NI increases and it took 9 months just to get an entry level position in a completely different field.

0

u/dustycheese 15h ago

are you me?! I’m in exactly the same situation

2

u/generichandel 14h ago

I'd wager there are many like us. Not much can be done other than seeing how it goes really.

18

u/adotg -2.38/-2.82 15h ago

A housing crash caused by different circumstances entirely.

It’s the other way round now. The housing crash in 08 caused economic trouble, now economic trouble is causing a housing price decline.

Regardless, the 0.6% drop in UK house prices per the article is a welcome correction

→ More replies (1)8

u/PALpherion 12h ago

all this wanking over 0.6%?!?! christ

call me when it's 40% please, then I might start calling it falling prices.

1

u/kill-the-maFIA 12h ago

You'd only start saying prices are dropping if price drops hit 40%? Lol

•

u/PALpherion 10h ago

DFS don't exactly advertise falling prices in their super january sales at 0.6% off, do they?

and those sofas are nowhere near as overpriced as housing!

10

u/lewispatty 14h ago

So the only solution is to keep inflating the price of a roof over a persons head?

10

u/fuscator 13h ago

Yes of course. Don't you see? It's the only way. Won't somebody think of the poor homeowners. We better protect them and all the landlords or else you're all "gonna get it".

3

3

u/Obvious_Yard_1846 12h ago

No, the solution is to have flatlined property prices and scrap stamp duty (which is itself inflationary as people tend to not sell unless the rise at least covers the stamp duty on the next house).

You don't need it to crash, you just need to let wages catch up.

→ More replies (1)1

u/mjc27 12h ago

Correct me if I'm wrong here but house prices are around 8x average wage so to get them back to the comfortable 3.4x average wage of the 1980s we'd need to more than double minimum wage. I don't think wages will ever catch up

•

u/Obvious_Yard_1846 11h ago

It's not quite that bad. The amounts might have been lower in the 80s, but interest rates were much higher (9-14%) so in terms of affordability it's not quite a question of just comparing wages to house prices.

If we saw a return to those kinds of interest rates with our current house prices though, we'd be completely fucked.

1

u/PALpherion 12h ago

on a social level the only solution is a hard crash, it's either coming now or later after we've fed it a bit longer.

on a personal level? get the absolute minimum you need in housing to survive and put as much as you can into mobile assets that will be affected less or still useful in a housing crash.

1

24

u/middleofaldi 15h ago

The harm has already been done by inflated house prices, we are just waiting for the inevitable correction and crash that comes with it

2

u/Tortillagirl 12h ago

Isnt the big issue that in 08 and with covid, the crash and correction were prevented by the government bailing them out both times.

-1

u/AkashicLogos 15h ago

The harm of inflated house prices is much, much lower than the entire economy crashing.

15

u/pantone13-0752 14h ago

The point is that the inflated house prices are what causes the inevitable correction and therefore the crash. You can't separate them and say 'haha, it's great when house prices are going up, inflated house prices are dandy and don't cause the economy to crash' and then when they come down again 'oh no, the entire economy is crashing, why is this happening, it definitely has nothing to do with those wonderful inflated house prices we used to have'.

31

u/middleofaldi 15h ago

A fall in house prices wouldn't cause a crash if the country wasn't insanely overleveraged in property assets. We have a huge capital misallocation problem because politicians have designed our economy on property speculation

https://henryfudgeofficial.substack.com/p/the-housing-theory-of-everything

0

u/generichandel 15h ago

if.

19

u/middleofaldi 15h ago

The more we allow house prices to inflate the worse the crash will be. House prices stagnating is the best way to delete the bubble without it taking the economy down with it

→ More replies (1)1

u/Jaggedmallard26 13h ago

You're arguing two things here, your previous comment says a crash isn't harmful then here you're saying a nominal terms stagnation is what we want. Those are two very different outcomes.

•

u/hu6Bi5To 9h ago

Not really. A fall in house prices is a one-off cost. Keeping house prices artificially inflated requires a continued cost year-on-year.

Just the economic costs of the decline of labour mobility within the regions of England over the past twenty years have been enormous.

But ultimately trying to claim one side of this market is somehow more virtuous than the other is a nonsense. Like any other market there's an optimal price and artificially deviating from that (whether by: planning controls, help to buy schemes, bailing out mortgage lenders) will prevent rather than assist that. Any pain that comes from natural market movements are still painful, but are just the sort of things that happen.

9

u/fuscator 13h ago

The more you apply these sort of motivated reasoning arguments to protect the haves, the more the have nots are just not going to care what happens.

Try telling generations of youngsters priced out of owning the same type of house as the generations before them that "we can't afford for prices to come down" and see where you get.

Every time I see this sort of argument my blood actually boils at the sheer selfishness of it.

8

u/Aerodye 14h ago

No but they will become more affordable

Your analogy to 2008 is ludicrous; 2008 was a credit crisis, not a little sell off in house prices

1

u/LongsandsBeach 14h ago

If people still sell.

If prices are falling some people will be put off from selling. Either because they can’t afford to due to negative equity, or they just don’t want to lose money.

Some people will still sell. But it’d be a smaller pool of available homes. Plus some people may be put off buying if prices are falling and they know they’d very quickly fall into negative equity.

3

u/alba_Phenom 12h ago

A housing crash that was triggered by a house price increase bubble... they were warned that house prices were spiralling out of control because they were giving everybody and anybody ridiculously unserviceable mortgages.

3

u/turbo_dude 15h ago

Disingenuous to say that it was triggered by a housing crash.

It was triggered by packaging up mortgages that should never have been issued as AAA credit risk in the US.

4

u/Minute-Improvement57 13h ago

2008 was triggered by bad debts and the crash in valuation of the debt packages. It wasn't triggered by the fall in the value of the building, the dip in house prices followed because the lending crunch meant fewer buyers in the market.

2

u/myurr 12h ago

They also fail to understand that the cost of building new houses has already been driven far too high by government policy regulations such that if house prices fall too much from their current level it will become uneconomic to build any new houses at all. The continued decline in demand for new builds will further squeeze existing trades and supply chains making any subsequent recovery even harder.

Our economic fortunes have been built on a house of cards since the late 90s - a lot of New Labour's economic "success" came from the asset price bubble that saw house prices treble in just over a decade, vastly outstripping average wage growth. We need to fundamentally rethink our economic policy. The country has been bumbling along despite policy for far too long, rarely because of it, and the constraints we've been building into the system are starting to come home to roost.

2

2

u/beenman500 13h ago

Housing crashes are bad. House prices leveling off for 10 years not so much though.

1

u/Critical-Usual 15h ago

Can you explain why/how?

8

u/PM_ME_SECRET_DATA 15h ago

Because the entire banking and finance sector is tied to property & people paying their mortgages. If people don’t pay their mortgages, banks are the ones who take the hit.

If banks die, whoops.

2008 was basically this. Everyone overleveraged to the tits on property.

Such a large part of our economy is housing that any crash would mean widespread unemployment and a severe decrease in the standard of living.

14

u/adotg -2.38/-2.82 15h ago

That is not what is happening here though. It’s a decline in consumer sentiment. The article talks nothing on increased default rates

-1

u/PM_ME_SECRET_DATA 15h ago

It doesn’t matter if it’s a decline in consumer sentiment as the cause.

If people end up in negative equity, the banks are now lending on an asset that isn’t worth what they have let people borrow.

→ More replies (1)7

u/Critical-Usual 15h ago

I can't see any correlation between your answer and your previous statement. House prices coming down does not stop anyone paying their mortgage

Also saying a housing crash would lead to unemployment... Based on what? Also the housing market hasn't crashed and there are no signs of it crashing, it simply went down slightly in price. It's really no big deal

→ More replies (1)2

u/JustCallMeLee 15h ago

I heard 45% of mortgages back then were NIV, non income verified. You could just state your earnings and the bank would take your word.

2

u/TaxOwlbear 13h ago

2008 was basically this.

No, it wasn't. Almost no banks died because they got saved with taxpayer money, and those responsible for the bubble suffered no consequences.

1

u/fuscator 13h ago

More and more people will see you arguing this and think "good".

If you keep always protecting the "haves", with this sort of motivated reasoning, eventually people are going to stop caring and just want the world to burn.

You're creating your own destruction.

•

u/brutaljackmccormick 9h ago

Not quite a crash, just a significant enough decrease that meant the logic of packaging up lots of 120% mortgages to people with a poor cedit rating and believing that the chances of them defaulting were completely independent events could no longer be plausibly supported by a majority of the market. (Note a minority of the market always believed it was bonkers)

1

u/Sakula90s 13h ago

Not mentioned the related industries , like furniture , house appliances, decorating and building materials, jobs for traders, and so on.

1

u/One-Web-2698 13h ago

We are basically hermit crabs. Used to be a factoid that the crabs line up to swap shells, with noone really reflecting that's exactly what we do as a species too.

106

u/Jaxxlack 15h ago

Who's idea was it to make our homes money making machines?

44

44

u/randomnine 15h ago

Short answer: Thatcher. Housing speculation for the majority was core to Thatcher’s domestic reforms with right to buy, limits on social house building, liberalising mortgage markets and so on.

The most pernicious part is Right to Buy. Thatcher’s government deliberately did this to reshape the electorate so we now have a democratic majority of homeowners - many of whom are counting on rising house prices as their retirement fund. This majority naturally votes in the interests of homeowners and landlords, so they’ve won every election since as far as housing policy is concerned up until perhaps 2024.

16

u/skywalkers_glove 14h ago

Absolutely. I couldn't agree more. Right to buy would have been fine if money that was made was reinvested into creating kit council housing. This didn't happen. On purpose

14

u/Jaxxlack 14h ago edited 14h ago

Same with alot of companies... They make profit but now want more and more and more because someone wants "growth".. why you're already winning?!!

See the. Downvotes are just confirming I call out shitty people n they don't like it..why? If you're so unaffected by your own lack of ethics thinking why try n shut up people calling you out.

→ More replies (2)•

u/WiseBelt8935 11h ago

An alternative idea: the systemisation of mortgages caused it. Back in the day, house prices were limited by what a guy working at the bank thought was reasonable. Then the system changed to one based on income ratios

24

u/skywalkers_glove 15h ago

Indeed. And there lies the elephant in the room. Too many people with god knows how many houses (not homes)have ridden the gravy train.

3

u/Lo_jak 15h ago

The parasite that is called Samuel Leeds.......

7

u/Jaxxlack 15h ago

Ohhh lol no we know it was Mrs Thatcher who said..here this is all our government buildings.. you can now sell these off for a profit..and won't ever have to worry again..

Oh and fuck the generations after you.

4

u/Lo_jak 15h ago

Its been a team effort really!

1

u/Jaxxlack 15h ago

Yeah there's a weird swathe in our society who don't understand why you SHOULDN'T be able to make obscene money from anything.. "hey ethics is your bag chum".. we all can make stupid amounts of money but our actual ethics stop us.. which is why that group feel just like a group of shitty people who want money not stability.

1

u/Aresbanez 12h ago

It's like that meme about what people think about landlords (as parasites) vs how landlords think about themselves (Jesus Christ). Leeds is taking advantage of a broken system openly and bringing awareness to it.

5

→ More replies (11)•

44

u/ZebraShark Electoral Reform Now 15h ago

Unfortunately I'm getting stung by this. No one's fault but we bought our flat in 2022 - since then it's gone down in value by about 5-10%. It's okay now, but any further and will be in negative equity. It is frustrating as now looking to move to a more long-term, permanent home.

32

u/MrBIGtinyHappy 15h ago

This is essentially the issue with wanting the bubble to burst, a lot of homeowners probably agree that prices should be more reasonable but unless banks forgive part of the loan (which they won't do off their own back) then a massive amount of the population end up stuck

27

u/gyroda 15h ago

Yep, what we need is a long period where prices grow less than earnings so we can "catch up".

15

u/richmeister6666 14h ago

Exactly, prices need to stagnate for a decade or so whilst earnings slowly rise up. The only way to achieve this is to build a lot more homes.

3

u/middleofaldi 13h ago edited 12h ago

We also need to address the policy side, bring capital gains taxes for property up to the levels of other investments, land value tax, stop buy-to-let mortgages etc

4

6

u/hicks12 15h ago

Yep it's why it's not a reasonable solution to just destroy the market overnight.

Need to focus on increasing supply to ensure prices slowly come down over time AND wage growth so with similar pricing it is still more affordable.

Too many will be caught in negative equity and could be in a worse state, sure it's part of the game and you can't be helped all the time but it should be a measured trend to improvement I think personally.

4

u/turbo_dude 15h ago

Lower house prices mean people need lower salaries to afford their mortgages means globally a more competitive workforce.

9

u/MrBIGtinyHappy 14h ago

Sure but you can't do that suddenly or a homeowner is left paying a 400K loan against a 300K house - doesn't matter what their salary is at that point, they'd have to get 100K of equity just to be able to sell/move

3

u/Jaggedmallard26 13h ago

And if they lose their job they have a very limited amount of time to find a new one (or spend all of their savings) before they end up homeless and bankrupt.

•

u/PALpherion 11h ago

right but that's the game, you know that when you sign up.

... don't you?

•

u/MrBIGtinyHappy 10h ago

No mortgage is stresss tested to a market crash though, I think ours was about 2.5x or 3x the monthly payment and that would still require considerable shifts.

2008 crash happened at around 20% default rate in the US

→ More replies (2)1

u/superioso 12h ago

Negative equity still isn't necessarily that big of an issue. It may still have cost less for your property to have gone down in value and you lost money in a sale than if you had just paid rent for years.

Investments in speculative assets to both ways after all.

3

u/MrBIGtinyHappy 12h ago

Negative equity isn't just losing money in a sale, it's paying value that doesn't exist. Keeping with my 400K mortgage analogy from another comment, a seller might be willing to accept a 300K offer but the lender still wants the other 100K left on the mortgage and now the seller has no asset and also no deposit so best case the seller is back into the rental market, worst case they're bankrupt.

I'm not advocating for the bubble to stay unpopped but it's also not a 1-2 year fix without mortgage forgiveness, it's potentially 5/10/15 years of needing house prices to decrease less than the rate of interest added.

•

u/superioso 11h ago

now the seller has no asset

This is why there's a minimum deposit of like 5 or 10%, so at least if there's a reasonable fall in price then at least their equity is very unlikely to fall below zero.

It's there's a drop of like 30% then the overall economy has bigger issues.

12

u/sylanar 15h ago

We've been trying to sell ours for over a year now. Can't lower the price anymore, it's already way less than we bought it for.

I'll probably have to try and rent it out, which I don't really want to do.

It's rough out there right now :(

7

u/PhysicalIncrease3 -0.88, -1.54 14h ago

'll probably have to try and rent it out, which I don't really want to do.

Bare in mind as soon as you do, you're liable for CGT which is probably going to end up at ridiculous levels soon

9

u/kryt4lp4l4ce 14h ago

I mean, you can always sell, it's just that sometimes you end up losing money.

3

u/TheFlyingHornet1881 Domino Cummings 13h ago

Not to sound too negative but checking Rightmove near me, some flats have leases that are unmortgageable. So you can only sell to a cash buyer, and currently the money's moving out of the rental market.

→ More replies (3)3

u/sylanar 13h ago

I'll already be losing money selling at the current listed price, I can't really afford to sell it any lower , or I won't have enough money to actually buy somewhere else

2

u/superioso 12h ago

Is the lost money the same as what rent would've cost you over the same time period, or is the lost money actually better than renting?

7

u/BonzoTheBoss If your account age is measured in months you're a bot 14h ago

It is frustrating as now looking to move to a more long-term, permanent home.

I hate being pessimistic, but you might want to start treating it as your "forever home" now.

I say this because this is essentially what happened to us. Our "starter home" has come our "forever home" because to move in to anything nicer or anywhere nicer, it's become unaffordable...

3

u/ZebraShark Electoral Reform Now 13h ago

So the few things going in our favour are:

My salary is significantly higher than when we bought our flat which has allowed us to have more options.

I have around £30,000 in savings which I've purposefully set aside for this.

I can now drive and have access to car, when we bought out flat this wasn't case so limited locations we could look to purchase.

Still difficult, and conscious many people are in much worse situations than myself.

4

u/bexxyboo 15h ago

Worried about this too! Bought my house in 2022, fixed term mortgage is up in mid 27, terrified that the money we've put into the house for it to be livable and not a dangerous leaking mess is going to have gone puff and we'll also be in negative equity with higher mortgage payments!

We bought in the hope of doing up, then selling on and downsizing/moving a bit further out of the city onto a long-term home.. that ain't gonna happen.

1

u/Jaggedmallard26 13h ago

I'm glad I ignored people telling me to buy something closer to my budget. Even I lose quite a lot of value I have the savings to pay off the entire remaining principle.

2

u/Bango-TSW Non-aligned cynic. 15h ago

Indeed. You just need to look back at the early 1990s to see just where this can go - especially if unemployment picks up.

14

u/evenstevens280 15h ago

Well I'm looking to buy out my ex-partner from their equity soon so this is good news for me 😂

40

u/richmeister6666 15h ago

It just had to deteriorate just as I stepped on the property ladder and my parents are looking to downsize their home, didn’t it?

18

u/Combat_Orca 15h ago

Your parents will still have made a lot of money off it

7

u/richmeister6666 15h ago

Very true! I’m sure they won’t complain, but I certainly don’t want to be stuck in negative equity.

5

u/jhrfortheviews 15h ago

In the same boat haha - what makes me feel better is that fundamentally people buy and sell in the same market so yes your parents might sell for less, but they should also get more for their money than a year or two ago when buying

9

u/HourChart 15h ago

You’ll be ok. The property market is for the long-term. A year after we bought our house it was worth £50,000 less than what we paid. We sold it 10 years later for 50% more than what we paid, and we’d built up equity all that time.

24

u/IEnumerable661 15h ago

The simple fact is that anyone with a decent property at the moment isn't selling unless they really need to! I and my neighbour would love to move, but we are not listing in this current economy. No thank you!

And I doubt we're the only ones.

The same happened after the 2008 crash. Nobody listed decent houses simply because they knew the buyers weren't there. Or at least, the buyers who were in a position to pay the asking price. So, simply sit, extend, improve, wait it out.

Of course, when those houses do come back on the market, suddenly house prices are "taking unexpected up turn!"

If banks are not lending, sellers aren't listing.

10

u/Master_of_Ocelots 14h ago

We decided to list ours a few months ago. Plenty of viewings, a couple of offers, but those fell through once the first time buyers revisited their mortgage broker and found they couldn't afford it any more. Ours is a 3 bed semi so those are our most likely market (with good schools etc nearby). Had a number of retired people looking to downsize, who have all complained its too small, which is frustrating as the photos are fairly representative and dimensions clearly shown 🤔

As the rate of properties coming to the market that we'd like have slowed right down we're mostly just sat pondering things. Considering just taking it off the market so we don't feel obliged to do viewings etc.

3

u/IEnumerable661 13h ago

Same with us. We want to upsize too. We didn't list, but looking at what offerings are there, it's mainly the scrap that nobody really wants in the first place with ambitious hole in the market pricing. The reality is, the decent houses just aren't getting listed. And it's because we all know full well, nobody's really buying.

•

u/Master_of_Ocelots 11h ago

We listed ours literally a week before it all went to crap. I keep reminding myself that we don't have to accept any offer we're not happy with and can take it off the market. I need to remind myself of any exit fees from the agent, but in fairness to them they've not pressured us to reduce prices to ensure a quick sale. They did tell us that houses around our price bracket were all falling in price to try and chase the first time buyers dropping, but that the houses we're looking to move in to were all refusing to lower their asking price.

Comically we got a letter from another agent we invited to value and didn't go with, the letter said about how they'd seen that our house was on the market for a while, listed a couple of reasons why, but they were basically all "cut your price 25% and it'll sell". Well, yes, but then we've just thrown a significant amount of our money away just to ensure your monthly turnover remains stable. No thanks.

Yep, the only houses we've been seeing are where the sellers are pressured to sell (so many divorces notably) or are coming out of probate. We'd be happy with the latter as they're usually nice houses, just need cosmetic work, but they have all been snapped up by cash buyers from conversations we've had with agents. Presumably to flip, says the grumpy man in me.

You've made the right choice sitting still.

7

u/XenorVernix 14h ago

I listed mine a few weeks ago and the buyers just aren't there. Couple of houses on my street sold like hot cakes in February before Iran war but the market has completely changed since then.

I don't have to sell but I'd like to upsize. I'd sooner take it off the market than accept a lowball offer because if prices are falling that much then so is the one I'm buying and I'm better off waiting it out. I'll get my next house cheaper, with a smaller mortgage and not pay interest between now and then. It doesn't make financial sense to upsize in a falling market.

•

u/Glittering_Vast938 10h ago edited 10h ago

Quite a few properties near me have been up for sale for a nearly a year now. These are big 5 bedroomed executive types with eye watering prices wanted.

•

u/XenorVernix 9h ago

I've seen some like that as those are the kind I'm trying to upsize to. Would take a 4 bed too though.

Very few of those executive houses are selling and the ones that do are getting several discounts. Some I'm watching get taken off the market without a sale.

Thing is if people like me can't sell their smaller houses to first time buyers or people upgrading to better 3 bed houses then the whole market stalls as I can't offer on those executive houses. One I'm watching has had a 5% discount in the last few days - I was happy to offer full asking price a few weeks ago if I had sold my house as I felt it was priced well. That one is no longer my first choice now as something I like more has come to market since.

2

u/csppr 13h ago

If you want to move, it shouldn’t make a huge difference? If your property is worth less than what you want for it, the same will apply to the property you want to move to.

Unless we are talking about buying a cheaper property. But in that case you need to weight it against opportunity cost.

2

u/IEnumerable661 13h ago

It makes a huge difference. If property prices are low in general, it makes a difference to your equity and interest rate. The bank would also be likely to question the home value so you need either the capital to make the shortfall valuation, or you need to keep looking.

5

u/PALpherion 12h ago

this is just the most blatant and naked mechanical proof that you're not buying a house, you're buying a financial product that you can sleep in.

how the hell can anyone trust property let alone with their entire life savings?

•

u/IEnumerable661 11h ago

... which the government will take off you if you fall ill in old age, or make it near impossible to keep with trumped up "care" costs.

9

u/KoMaMcNoob 15h ago

It is somewhat bewildering that a significant chunk of this is leasehold flats, especially in London, causing knock on effects. Policy on this is dire and we are at if not past the canary in the coalmine situation.

Luckily for average numbers, because no one wants to buy into massive service charges people aren't buying/downsizing so much so doesn't look and feel as bad as it is... This trend will carry on though for the next few years.

25

u/parkway_parkway 15h ago

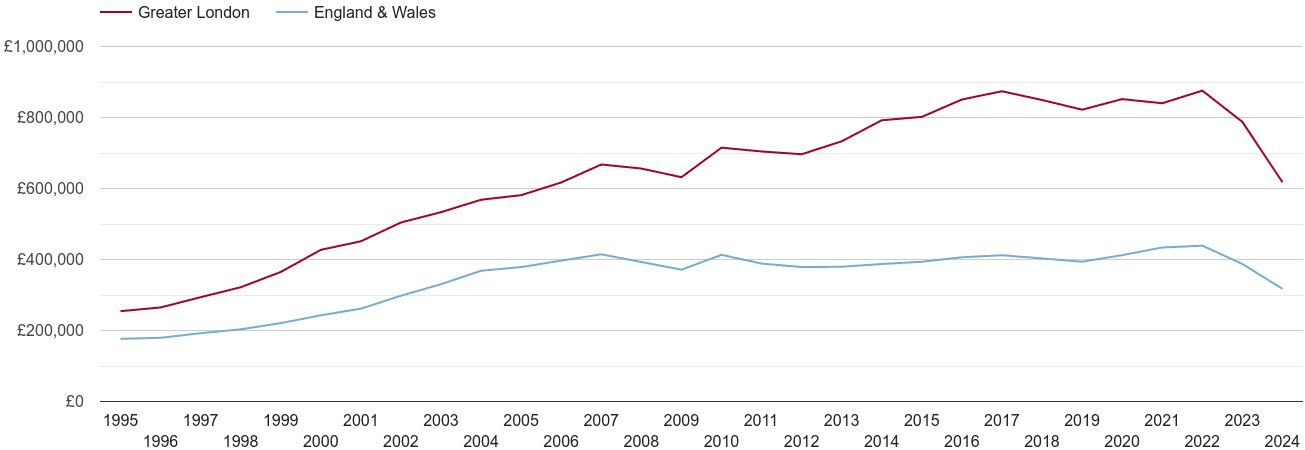

Data here says London is in the midst of a massive crash, in real terms prices are down 30% and in nominal terms prices are falling steeply.

It's understandable, the whole thing was a bubble based on terrible economic fundamentals and it's easy to see everything falling 30% in nominal terms or more to get back in line with affordability.

4

u/kryt4lp4l4ce 14h ago

Where did you get 30%?

1

u/parkway_parkway 14h ago

The real terms 30% fall is from £920k to £630k adjusted for inflation.

The other 30% is just a guess about how messed up the UK economy is now, how there's much less immigration, how foreign investors don't want to be in a city where prices are falling and how birthrates are low.

3

u/Salty_Salamander2555 12h ago

It’s mostly flats that are basically unsellable because of leasehold issues and extortionate ground rents/service charges

3

u/parkway_parkway 12h ago

If you scroll down a bit more some of the biggest falls have been for detached houses.

-3

u/One-Air-571 15h ago

My completely unevidenced theory is that London is possibly the most exposed city in the world to AI; thus, uncertainty re 'will I replaced be AI' is a major drag on the housing market.

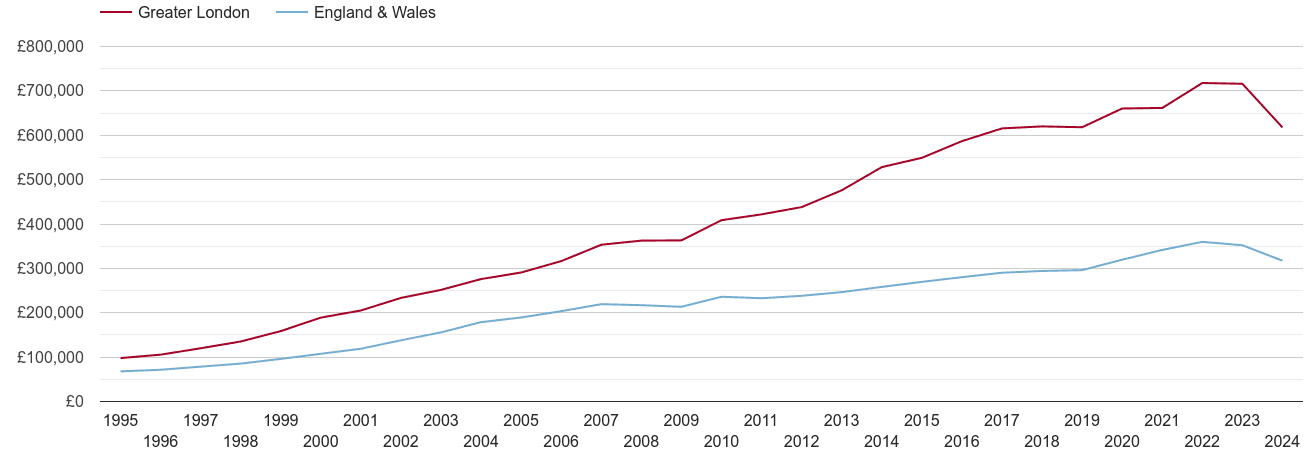

Correlation is not causation, but interestingly the charts you've shared here show the peak right in late 2022, when AI was launched. Obviously it would have taken a 1-2 years for this anxiety to feed through, so maybe AI didn't signal the initial decline, but might now be helping it.

6

u/digitwasp 14h ago

I think there's a more obvious answer than AI anxiety: mortgage rates skyrocketing after the disastrous Liz Truss premiership. A house that might have been affordable at 2% interest is less so at 6% interest.

The Iran war has sent mortgage rates back up again, and prices are unsurprisingly falling again.

2

u/TheFlyingHornet1881 Domino Cummings 12h ago

London is also heavily affected by the issues wuth leasehold and cladding on flats, a lot are unmortgageable and there's not a lot of cash buyers out there.

2

u/Jaggedmallard26 13h ago

A lot of it is also that London has a lot of high rises that are now worthless under post-Grenfell legislation.

16

u/ItalianCoffeeMorning 14h ago

Having only recently purchased a house. Being a millennial it seems about right for the market to dump and for us to be left with negative equity. Just a cherry on the top of the years and years of hard work

→ More replies (1)5

u/pandahunter 12h ago

hell yeah brother. bought a one bed in 2020 just before the pandemic. now i have a kid and a partner who can’t afford to go back to work, we are FUCKED. moved about 11 times across flatshares before buying and looks like i’ll be living in a cupboard for the foreseeable

12

u/redunculuspanda 15h ago

Looking to downsize my mums place at the moment and it’s looking bleak. Ultimately i guess it doesn’t matter to us that much if we get less, if the place we want to buy also drops appropriately.

20

u/GhostCanyon 15h ago edited 8h ago

the thing i don't understand about the fear around housing market crashes is that say my house goes down 10% in value then surly the house i want to buy also goes down 10% in value so the only people set to lose mout are people who own houses purely as financial asset. even if my house dipped into negative equity then yea loosing the ability to move in the next few years would be annoying but its still my house and as long as i can afford the mortgage i can stay in it and pay the mortgage the same way id intended too all along

12

u/turbo_dude 15h ago

True but if you have mortgage commitments which now exceed the value of your home, how are you going to finance the new purchase because you’re now in debt even after selling the existing property.

It’s like having a negative deposit.

7

u/GhostCanyon 14h ago

yea i get that, in that case you would need to stay in the house and pay the mortgage until you got into positive equity the same way you do with a car on a PCP. its rubbish and not a good situation for anyone to find themselves in but the media make out that a fall in housing costs is the end of days when really its only a problem if you're super rich and you use housing to park you money in an asset that's not aloud to decrease in value ever?

→ More replies (2)3

u/ticking12 14h ago

It assumes the status quo of you being stuck in that house is both tenable (what if you lose your job?) and desirable (what if you are offered a better paying job elsewhere or have a growing family)? In either outcome that 10% (or more) is suddenly painful. Good policymaking is generally you want as little friction in people moving house as reasonably possible (which is why stamp tax is a bad tax).

To be clear I'm of the opinion that a gradual deflating of the market is a good thing, but it's going to have to be gradual (demographic change permitting - as with less people we may suddenly find ourselves with less demand).

•

u/GhostCanyon 11h ago

What if you loose your job any time? Yes you can sell your house if you’re not in negative equity but it still might take a year to sell. Life is a gamble. Property should not continually go up in value 10/20/30% a year it’s insane. The government created an asset that is risk free and can only go up in value. Thats not sustainable for the people who need to buy those assets to have a home

•

u/ticking12 10h ago

I feel like you hit me with a stock answer? I wasn't saying saying property should go up 10/20/30% in value.

The context for this discussion is that property prices have been dropping in real terms (i.e. Not risk free).

https://i.plumplot.co.uk/London-real-house-prices.png https://i.plumplot.co.uk/London-house-prices.png (and dropping/stagnating in nominal terms).

Both are fine so long as the value drops are not so large people are being outpaced by their loans, which was the whole point of my gradual deflation point?

The specific problem with these value drops is that they are mostly a result of mortgage rate increases and a weak economy rather than supply so unfortunately affordability hasn't particularly improved.

2

u/TheAlmightyTapir 12h ago

You're bang on the money, it's the same as when rents go up because of this and/or the renters' rights bill and people come here smugly going "hmmm you see, guys, it's stupid to want to improve things for people".

The fact we had house prices going up like 20% a year and landlords could just kick out tenants for no reason and overleverage everything to get even more properties should just be accepted as the status quo and the problem allowed to get worse and worse and worse and worse until a 2% decrease in house prices causes the FTSE to fall off a cliff.

We cannot POSSIBLY have a correction in house prices. We need to keep the landlord class happy. (/s)

EDIT: Also bonus points for this article being about how price growth has SLOWED annually, not even that house prices have decreased annually, and people are still in here talking like it's the end of the world and everyone will be in negative equity.

•

4

u/Jaggedmallard26 13h ago

long as i can afford the mortgage i can stay in it and pay the mortgage the same way id intended too all along

THIS IS THE PROBLEM. You are assuming that during market downturns everyone will keep their jobs. If you are close to your affordability limit then if you lose your job you are fucked.

→ More replies (1)•

u/iamnosuperman123 10h ago

People are unlikely to sell/can't sell due to having less equity to move on with. People might celebrate a house market crash but all it does is stop people moving/buying until the market picks up again

•

u/GhostCanyon 8h ago

What about the people who’ve been trying to afford a house who become able to?

•

u/iamnosuperman123 8h ago

They won't be houses to buy as supply retracts. Stamp duty and other associated cost with buying a selling is such a killer that people need equity in their homes to sell. People will wait it out.

We have to understand why house prices are falling because that reason will dictate if house prices falling is a good thing or not (i.e is it interest rates or the doom and gloom of a possible recession due to low growth)

{kind=link}

{kind=link}

9

u/Obvious_Yard_1846 13h ago edited 13h ago

Hahahahaha. I want to sell at the moment as we've outgrown our house. Had the estate agents round last week.

Why does it feel like, as a millennial, every big financial decision in my life always ends up at the worst time?

I'm probably looking at a £20k loss, then all the other moving costs on top (so maybe another £15-£20k on top of that). Fuck this country- it doesn't have to be this way. The government could at least stop profiting off our misery with fucking stamp duty.

It's not like I live in a fucking mansion, it's a 3 bed railway worker terrace. Can we get a fucking break?

→ More replies (4)8

u/sbeveo123 12h ago

Guarantee the state pension will vanish the moment it comes time for millennial to retire.

3

6

u/GlumAd9856 15h ago

This is a good thing. If only the Labour government was serious about planning reforms and building new houses, this would have been the opportunity to lock in house price stagnation for decades to come.

2

u/MysteryWra 12h ago

Falling house prices? Even reform (tory-lite) will bring in waves of migration if that ever happens (sigh)

2

u/Aware-Line-7537 12h ago

When electronics prices or oil prices fall, I don't see people use "deteriorate".

•

6

u/Combat_Orca 15h ago

Expected this during the ridiculous highs of the pandemic but kept getting told I was wishing for a crash as believing house prices don’t keep going up constantly apparently is wishing for a crash. They’ve been stagnant or lowering for a while now to correct that price spike.

2

u/doubleheman 14h ago

Isn’t this quite localised problem, in my area house prices have either increased or stayed relatively the same

2

u/MrScaryEgg 15h ago

One of the few things that elicits some sympathy from me for the current government is the fact that we apparently all want low inflation and a more reasonable cost of living, but we also don't want prices to come down.

2

u/Dijstraanon 15h ago

This is amazingly good news. House prices are to high and need to come down and stay down.

•

0

u/catgod888 15h ago

It’s not Iran. It’s the renters rights act. Many people are getting out.

5

u/m1ndwipe 15h ago

The generally higher interest rates are definitely Iran because of the inflationary pressure on energy prices.

But I think some level of supply increase from a one time disposal of some properties due to the Renters Rights Act might be contributing a little bit.

•

u/angryratman 11h ago

High rates were already there and have been for a few years now. Iran has just meant that rates haven't and are unlikely to come down anytime soon.

1

u/catgod888 15h ago

Speak to anyone in the industry. An enormous amount of proprieties have gone on the market in the last 6 months and can’t be shifted.

2

u/m1ndwipe 14h ago

I mean I did acknowledge that it's happening to some extent, but obviously stubborn interest rates are not helping, and those are definitely caused by the inflation situation which is why the rate cuts everyone was expecting this year haven't materialised.

1

1

u/Kee2good4u 13h ago

House prices are linked to interest rates, simple as. There is just a delayed link. Interest rates go up, people can afford to borrow less money, people offer less money on houses, house prices decrease.

It's why the comparisons to house prices decades ago with much highier interest rates, compared to the really low interest rates a few years ago already really annoyed me, as it missed other key variables.

In real terms house prices have dropped considerably since interest started going up from 2%.

•

u/AutoModerator 15h ago

Snapshot of House prices fall again as property market ‘deteriorates’ submitted by signed7:

An archived version can be found here or here. or here

I am a bot, and this action was performed automatically. Please contact the moderators of this subreddit if you have any questions or concerns.